The Great Digital Myth: A Speculative Rant on How Software Killed American Progress

A loosely-structured stream of half-baked thoughts on software, artificial intelligence, infrastructure, economics, venture capital, and the future of humanity.

Bubbles are built on myths. Rather than making them fragile, this makes them tremendously robust and enormously resilient. The stories we tell ourselves become our ground truth regardless of whether those stories are fact or fiction.

A recent piece in The Economist noted that some prognosticators are predicting AI, specifically Artificial General Intelligence, could drive annual GDP growth to 20% to 30%+ per year. Moreover, because AI can accomplish this without the need for more people—unlike the agrarian and industrial societies of generations past—GDP per capita should also balloon. What’s not to like? AI, the panacea for our times, here to usher in a utopian society where everyone is healthy and wealthy.

Such Pollyannish sentiments closely parallel the rhetoric from the dot com boom. New millionaires were being minted daily. Fundamentals didn’t matter. Stratospheric valuations still seemed underpriced. The internet and its growing number of websites would usher in a new era of prosperity, redefining the Good Life and changing forever how we live it. And it did. The advent of the Information Age and the proliferation of software have fundamentally improved life for everyone, everywhere, forever.

Or, so the Great Digital Myth goes.

Such sentiments constitute myths, not necessarily because they are false, but because they represent a cultural premise that shapes what we believe and how we behave. Unfortunately for the Great Digital Myth, there is an increasingly obvious body of evidence suggesting that information technology as we know it today has actually contributed to the deterioration of wealth and health in America. Now, this statement is bound to be controversial to many policymakers, investors, technologists, tech entrepreneurs, and believers in American Exceptionalism in general. I admit that this is a largely non-consensus view, but hear me out.

Some commentators have argued that AI is already having a positive impact on economic data. AI investments are essentially propping up a sluggish private capital market, with valuation levels teetering on “unhinged.” AI has also been the primary driver of public equity performance recently and will likely boost GDP in the coming quarters. But metrics like corporate earnings, stock performance, GDP, and GDP per capita can be terribly misleading. These measures are indicators of overall economic health, but say nothing about the social, economic, and physical health and wealth of individuals and households.

Indeed, I would argue that increasing investment in digital technologies and software since the advent of personal computing in the 1970s has crowded out investment in infrastructure and fixed assets that enable physical productivity, socioeconomic mobility, and a more connected culture. It should go without saying that infrastructure is essential to a healthy economy and a vibrant society. Our built environment literally shapes our world and how we experience it. While infrastructure is often seen as static, infrastructure and fixed asset innovation (think next generation energy and transportation technologies and 3D printing and additive manufacturing, for example), have the potential to transform the world we inhabit, for everyone.

In their new book, Abundance, Ezra Klein and Derek Thompson blame bureaucracy for constraining supply dynamics that would otherwise made building physical systems like infrastructure and housing more affordable. While there is some truth to this, I also believe that the fixation on software has had a catastrophic opportunity cost: investment in tangible technologies, hardware systems, and critical infrastructure that could have transformed how we produce and distribute energy, build houses, create access to essential resources like food and healthcare, manufacture and move goods, and connect people to healthcare, employment, and other people.

Yet, U.S. public infrastructure spending as a share of GDP continues to fall and is nearly the lowest it’s been in 50 years. U.S. Gross Fixed Capital Formation, a measure of the amount invested in fixed assets, has long been in decline and has lagged significantly behind China since the 1970s. As is widely known, domestic manufacturing productivity has slowed over the last 15 years after decades of significant growth. The reasons for this slowdown are complex and involve not only global competition but also capital equipment investment levels and financial asset allocation. I believe one reason is that we stopped investing in hardware innovation. While it’s true that manufacturing R&D is up, much of this spending has been focused on digital transformation rather than hardware innovation. Using software to make processes more efficient can only get you so far. At some point, the entire method has to change. But you can’t truly transform how you make a physical product without physical transformation.

Theoretically, private spending should have filled these critical gaps, as is often necessary and occasionally observed in less developed nations. Yet, the opposite has happened. Private investment in infrastructure and fixed assets has declined precipitously decade over decade as investment in software and intangible assets have soared, along with wealth inequality.

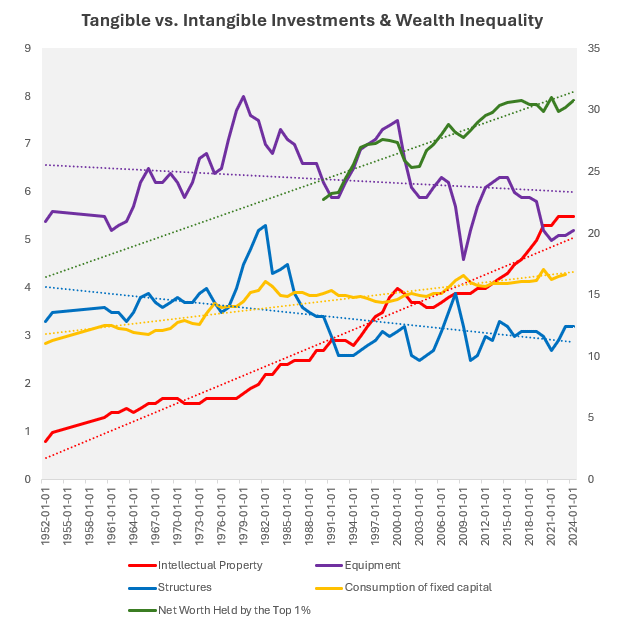

Figure 1 below shows private investments in structures and equipment as a share of GDP (purple and blue), private investment in intangible IP assets such as software as a share of GDP (red), the consumption rate of fixed capital (yellow), and the share of net worth held by the top 1% (green).

We can see that in the late 1970s, private investment as a share of GDP starts a multi-generational decline while investment in IP starts to accelerate. The same Federal Reserve Economic Data (FRED) dataset demonstrates that the expansion of investment into IP is primarily driven by software. This decline in fixed asset investment is exacerbated by rising Consumption of Fixed Capital (CFC), which measures the decline in the value of fixed assets from things like wear and tear and obsolescence. The higher the CFC rate, the more fixed assets are being devalued. What’s interesting is that the U.S. GINI index, a popular measure of economic inequality, rises commensurately with increasing software investment. The parallelism between these two lines here should be interpreted cautiously as the GINI coefficient is measured on an entirely different index than these other metrics. Nevertheless, despite fluctuations related to macroeconomic booms and busts, inequality continues to rise as software investment increases and investment in infrastructure and fixed assets declines.

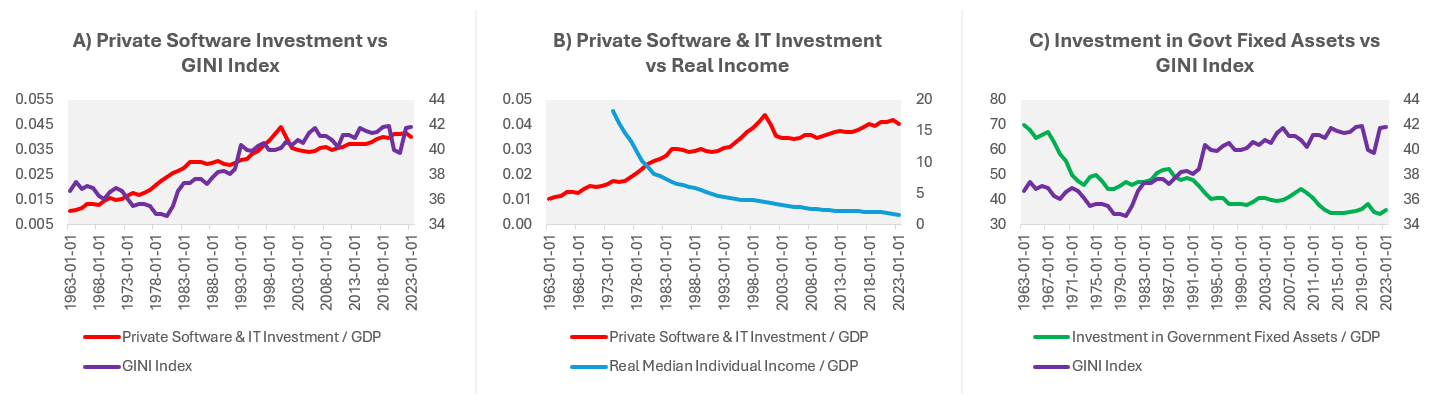

In Figure 2 below, chart A shows private software and IT equipment investment as a share of GDP relative to the GINI index. Chart B shows private software and IT investment relative to real individual income as a share of GDP. Chart C represents public (government) investment in fixed assets as a share of GDP relative to the GINI index. When the Y and Z axes are roughly leveled, we can see some interesting—but not necessarily causal—correlations. As private investment in software goes up, so does inequality. As private investment in software goes up, incomes go down. As public investment in fixed assets goes down, inequality goes up. Again, as with Figure 1, there seems to be a decoupling in the late 1970s that establishes a new correlation that largely holds to the present day.

Let’s assume, as a thought experiment, that there are causal correlations here. The most obvious conclusion would be that the increase in the share of economic resources being allocated to software investment, which started as the benefits of the Information Age became publicly available, depresses incomes and drives up inequality, particularly in the absence of public investment in infrastructure to support socioeconomic opportunity and wellbeing.

There is no doubt a confluence of political and economic factors impacted these trends. Frequently cited culprits include high inflation in the 1970s, a renormalization of the post-WWII economic boom period, increasing globalization, the end of the gold standard, de-unionization and deregulation, as well as others. It is largely acknowledged that something happens in the 1970s that begins hollowing out the American middle class and results in a host of negative long-term trends. Less frequently discussed, however, is the role that the Information Age, the advent of personal computing, and growth of the software sector may have had in causing or accelerating these trends, even if that role was to reduce or redirect investment that would have otherwise went into infrastructure and hard tech.

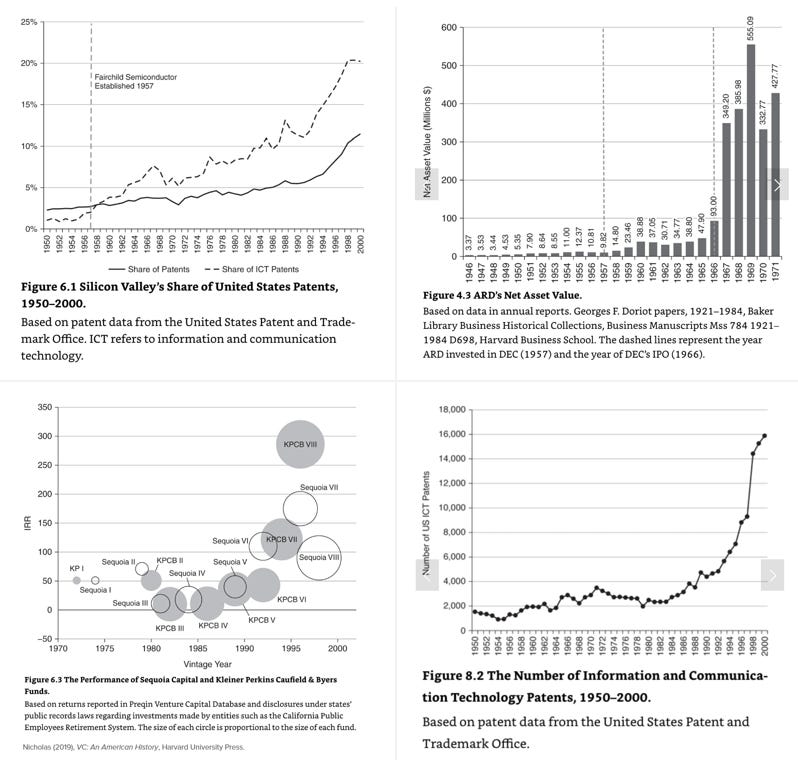

At the same time information technologies were making their way from the lab to the market, another industry was on the rise: private risk capital. Although the early iterations of venture capital arose after the Second World War, it wasn’t until the 1960s when the fund model we know today was devised. Tom Nicholas does an excellent job of chronicling the emergence of private risk capital models in VC: An American History. 10/10 highly recommend. Historical VC data tells the story well.

What we see in the four charts that comprise Figure 3 is information technology related patents surpassing patents for other forms of innovation by 1960 and then accelerating more aggressively in the late 1970s (upper left), when the value of digital investments started skyrocketing as demonstrated by the net asset value of American Research and Development Corporation, which is largely considered the first VC firm. We see the performance, size, and number of Sequoia and Kleiner Perkins (both major longstanding VC groups) funds grow through this period, leading to the late 1980s when digital technology patents start soaring into the dot com boom. Public equity market capitalization by sector also demonstrates the rise of digitally-focused investment patterns starting roughly around this period, but VC is typically the asset class that is most interested in funding higher-risk innovations with transformative potential.

Venture capitalists love software for its scalability characteristics. Rapid revenue growth can fuel superlinear margin expansion, generating capital efficient companies with high IRR yielding potential. Hypothetically, investments in digital technologies past and present should have yielded tremendous and broadly distributed benefits for businesses, individuals, and society. In some cases, this is undoubtedly true. The internet, for instance, is inarguably a General Purpose Technology (GPT; not to be confused with Generative Pre-trained Transformer), or technologies that have an infrastructure-level impact on an entire economy. But the internet wasn’t funded by visionary venture capitalists, but by the U.S. government. While the private sector occasionally innovates a GPT, such as the combustion engine and the transistor (although Bell Labs was founded with a government grant), most of the technologies that can be validly considered GPTs are largely government funded. This stands to reason given these technologies are typically far more complex than your average iPhone app—and, interestingly, they are most often NOT software.

While the internet leverages software to function, it is principally a network of physical devices supported by physical hardware such as servers, switches, routers, and internet exchange points. Think of history’s greatest GPTs: gunpowder, the steam engine, the printing press, the automobile, telephony, the airplane—all hardware. Many technologists and VCs are arguing that AI is a GPT. Some historians and economists, including some at the Federal Reserve, have their doubts.

Even if AI is a General Purpose Technology the current flavor of generative AI is unlikely to be able to repair the generations of damage we’ve done by ignoring physical GPTs in favor of software-based applications. Additive manufacturing is a prime example. Had we continued to invest in 3D printing technology, we may have been able to provide the abundant affordable housing that Ezra Klein and Derek Thompson talk about in their book.

Additionally, even if AI unlocks heretofore unseen economic growth, who will benefit from such growth? If the thought experiment posed based on the data above is any indication, it is likely that only a well-positioned few will see any material benefit from AI. Sure, like all software, AI may make our lives more convenient, a little easier, a little more entertaining, but are they making our lives better?

Despite what some highly self-interested companies and CEOs have said, AI is more likely to be a net job destroyer than net job creator. I have long been frustrated with executives who, in public, say that AI is not going to take anyone’s job while, in private, they identify the cost reductions they can achieve by replacing employees with AI and automation. Fortunately, the truth is finally coming out as an increasing number of execs come clean and the data starts cutting through the delusional and deceptive Pollyannish rhetoric.

At the same time, loneliness is on the rise. We’re more connected to people, information, and ideas than at any prior point in history and yet we’re more lonely than we’ve ever been. Some recent studies have suggested anywhere from 40% to 50% of Americans suffer from frequent loneliness, with more than 20% reporting serious loneliness. Unsurprisingly, studies have found digital media play a role in exacerbating loneliness. You don’t say.

Relatedly, new research reveals that levels of conscientiousness have fallen significantly over the last decade among those aged 16-40. This group has become materially less extroverted, more neurotic, and less agreeable. This doesn’t seem surprising when you consider most people today experience the world through their phones. They travel through social media. Solve their problems through ChatGPT. Meet people over Zoom. Find love on OnlyFans. Are we even human any more?

Despite these maladies, the investor class responsible for fomenting innovation continues to support digital apps designed to trap us in this paradigm, where we can be tracked and sold to, where we can lose ourselves while losing our humanity. And the general purpose innovations and fixed asset investments that would help truly connect us in the physical world, build cheaper homes, supply more abundant energy, access healthier food and ever-better healthcare, and create jobs and opportunities that will yield a broader distribution of benefits, nobody is investing in those. They’re too hard. The holding period too long. The R&D risk too high. Risk capital is no longer interested in real risk, or isn’t willing to take risk on the things that matter.

Say what you will about Alex Karp’s The Technological Republic, but he is right to point out that the origins of modern venture capital and information technology are very much rooted in the pursuit of higher ideals, particularly the defense of our nation. Indeed, the Department of Defense was the creator, funder, and/or customer for many of the early information technologies that drove the trends seen in the charts above.

Today, we desperately need to invest in our national defense once again, not to protect ourselves from a foreign adversary, but to protect ourselves from ourselves, to rescue our citizens from the digital addictions we have created and reveal Great Digital Myth for what it is: a lie. Your life is out there, in the world. You are an embodied creature who needs an embodied experience. Instead of investing in yet another digital delusion, let us invest in new modes of transportation that will take us new places. Let us invest in new social infrastructure that will connect us with new people. Let us invest in better construction tech that will allow us to build a better world. Let us invest in new life science that will help us live longer. Let us invest in new sources of power that will power the next generation of ideas. Let us invest in the general purpose innovations that matter so that in our attempts to make artificial intelligence more human we don’t end up making humans artificial.